Where are hotel rates climbing in the USA? Where are rates dropping? Hint: not many places.

HotelNewsNow.com hotel industry data from Smith Travel Research confirms one fact about hotel rates that I had intuitively discovered by my own observations: San Francisco hotel rates skyrocketed faster than any other location in the US in 2012.

Smith Travel Research (STR) is the Tennessee based hotel data industry firm. Many of yesterday’s statistics from the pwc report I cited in Thoughts on Europe 2013 pwc hotel forecast were based on STR data analysis. STR and STR Global data is published in industry reports and through their media outlet HotelNewsNow.com. Data published below is from Smith Travel Research hotel industry presentations.

USA Occupancy

USA hotels averaged 90 million room nights each month in 2012 with 147.4 million room nights available. December 2012 set a seasonally adjusted record of 91.7 million room nights. Yet total hotel occupancy is around 61.4% to 62.2% and the peak years of 2005-06 touched 65% occupancy. There are more hotel rooms now than there were in 2006. The US has 1.8 billion room nights to fill and room demand is currently about 1.1 billion room nights. There are lots of empty rooms every night across the USA.

- 2011 Hotel Occupancy grew 4.2%.

- 2012 Hotel Occupancy grew 2.5%.

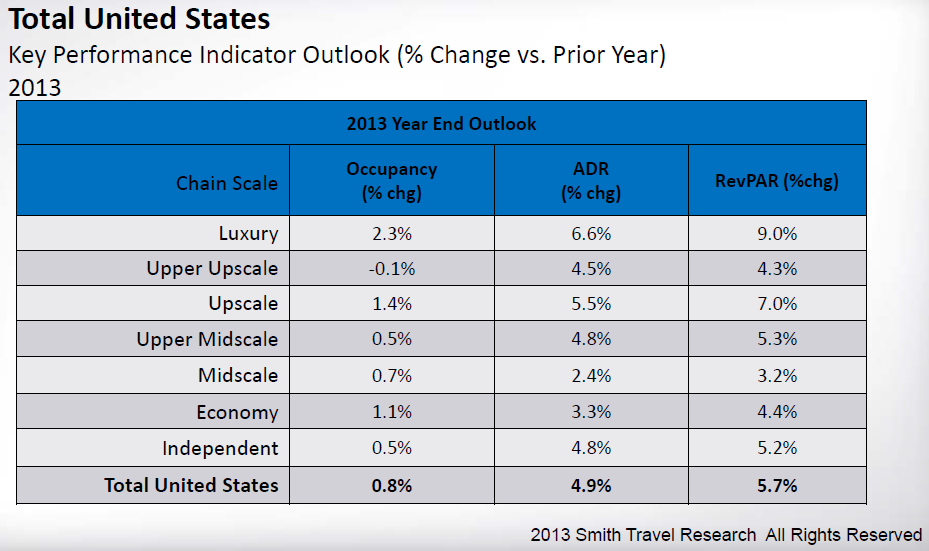

- 2013 Hotel Occupancy forecast to grow 0.8%.

- 2014 Hotel Occupancy forecast to grow 1.3%.

Hotel occupancy is predicted to grow for US hotels, but at a much slower rate than the past two years.

So why are US hoteliers partying like it is 2005?

Hotel Rate

Hotel Rates in the USA are forecast by Smith Travel Research to grow over the next two years.

- 2011 US Hotel ADR grew 3.8%.

- 2012 US Hotel ADR grew 4.2%.

- 2013 US Hotel ADR forecast to grow 4.9%.

- 2014 US Hotel ADR forecast to grow 4.6%.

Average Daily hotel rate measured by ADR at $106.89 year-end 2012 is positioned in 2013 to surpass the previous rate peak for US hotels of $107.03 from 2008.

The average US hotel room rate that dropped to under $100 in 2009-10 is positioned to see ADR of $116 in 2014.

Seven of the Top 25 Hotel Markets in the USA during 2012 surpassed their previous record high room rates. New Orleans and San Francisco are the two notable regions.

- San Francisco (+$15.03; +9.6%)

- New Orleans (+$13.05; +10.9%)

- Oahu (+$10.81; +6.3%)

- Boston (+$1.99; +1.4%)

- Nashville (+$1.31; +1.3%)

- Miami (+$1.31; +0.8%)

- Los Angeles (+$1.07; +0.8%)

18 of the Top 25 Hotel Markets in the USA at year-end 2012 are still below their peak room rates.

- St. Louis (-$1.27; -1.5%)

- Norfolk (–$3.02; -2.7%)

- Anaheim (-$3.35; –3.4%)

- Minneapolis (-$3.86; -3.8%)

- Philadelphia (-$4.24; -3.4%)

- Denver (-$5.38; -5.1%)

- Atlanta (-$6.04; -6.6%)

- Houston (-$6.37; -6.3%)

- Seattle (-$6.53; -5.1%)

- Tampa (-$8.25; -7.8%)

- Detroit (-$8.38; -9.5%)

- Dallas (-$8.40; -8.9%)

- Chicago (-$8.41; -6.3%)

- Orlando (-$10.40; -9.7%)

- San Diego (-$11.21; -7.6%)

- DC (-$12.09; -7.9%)

- Phoenix (-$19.74; -15.7%)

- New York (–$31.02; -11.0%)

Hard to believe New York is 11% below its peak rates after seeing the rates for hotels in September 2012 when I stayed at the W Union Square ($650 per night after tax) and Westin Times Square ($450 per night after tax).

Chain Scale Market Segment 2013 forecast Smith Travel Research.

Luxury hotels are expected to show strong performance in 2013 with ADR increasing 6.6% and occupancy increasing at a higher rate for luxury hotel market segment compared to all other hotel market segments.

Luxury hotels are not where the new hotel growth is happening. The real growth is in the Midscale and Upscale hotel brands.

Top 15 Brands for New Hotels in 2013 (Smith Travel Research data)

- Holiday Inn Express 18,701 rooms

- Hampton Inn & Suites 17,698 rooms

- Courtyard 14,302 rooms

- Residence Inn 13,782 rooms

- Hilton Garden Inn 12,159 rooms

- Fairfield Inn 10,450 rooms

- Holiday Inn 10,357 rooms

- Homewood Suites 8,675 rooms

- Home2 Suites, 7,350 rooms

- Hampton Inn 7,131 rooms

- SpringHill Suites 6,905 rooms

- La Quinta Inns & Suites 6,179 rooms

- TownePlace Suites 6,064 rooms

- Candlewood Suites 5,997 rooms

- Comfort Suites 4,931 rooms

The big hotel chains will get bigger in 2013. Part of this is due to the ability of hotel projects to get better financing when a brand name is associated with the business construction project.

Hilton Worldwide: 53,013 rooms

- Hampton Inn & Suites 17,698 rooms

- Hilton Garden Inn 12,159 rooms

- Homewood Suites 8,675 rooms

- Home2 Suites, 7,350 rooms

- Hampton Inn 7,131 rooms

Marriott International: 51,503 rooms

- Courtyard 14,302 rooms

- Residence Inn 13,782 rooms

- Fairfield Inn 10,450 rooms

- SpringHill Suites 6,905 rooms

- TownePlace Suites 6,064 rooms

InterContinental Hotels Group: 35,055 rooms

- Holiday Inn Express 18,701 rooms

- Holiday Inn 10,357 rooms

- Candlewood Suites 5,997 rooms

La Quinta Inns & Suites is owned by Blackstone Group, the same owners of Hilton Worldwide.

Ric Garrido, writer and owner of Loyalty Traveler, shares news and views on hotels, hotel loyalty programs and vacation destinations for frequent guests. You can follow Loyalty Traveler on Twitter and Facebook and RSS feed.

2 Comments

Comments are closed.